The impact of EU sanctions on Russia visualised and explained in infographics

The Hungarian government launched a National Consultation survey on “failed sanctions against Russia” in mid-October, even though Hungary has voted in favour of all the sanctions packages. The deadline for completing the questionnaire was 15 December. In this article, we go through the survey questions and also look at the impact of EU sanctions on the Russian economy and trade.

The Russian invasion of Ukraine on 24 February 2022 marked the beginning of the Russian-Ukrainian war. In response to the invasion, the European Council has imposed a series of sanctions this year, aimed at making Russia’s situation politically and economically more difficult, while at the same time reducing the continent’s dependence on Russia for energy.

On 14 October, Hungary’s government launched a national consultation on “sanctions against Russia”, which the government consistently describes as a failed measure. The consultation asks Hungarian citizens for their views on the importance and effectiveness of EU sanctions, mainly on energy carriers, in the form of seven questions.

The so-called “national consultation surveys” are letters sent to every Hungarian household on behalf of the government. In recent years, the Hungarian government has used this method on several occasions to ask people’s opinions on issues such as COVID-19, George Soros, or immigration. The latest national consultation cost nearly eight billion HUF.

The Hungarian government has consistently rejected sanctions in its communications.The result of the consultation – which as usual is expected to reflect the government’s views, mainly because of the manipulative questions and the wording of the expected answer – does not count for much as far as the existence of sanctions is concerned, as their adoption required the unanimous agreement of all EU member states, including Hungary. So the Fidesz government itself voted for the EU sanctions, which it is now condemning on billboards and in the consultation.

The seven questions are about oil imports, gas imports, imports of solid fuels (such as coal), imports of nuclear fuel, the expansion of the Paks nuclear power plant, the tourism sector and food supply.

1. Oil sanctions

The first question concerns the ban on imports of crude oil and petroleum derivatives adopted in the sixth sanctions package. In order to maintain the country’s oil supply, the Hungarian government has requested that Russian oil can continue to be imported by pipeline instead of a full embargo. This was successful, the embargo now only applies to maritime shipments, which account for 90% of Russian imports. The European Council has also adopted the G7-initiated price cap, under which EU companies can only participate in the maritime transport of Russian crude oil or petroleum products to countries outside the EU if the price of the shipment is equal to or lower than the price cap.

Hungary is not affected by either the embargo or the price cap,

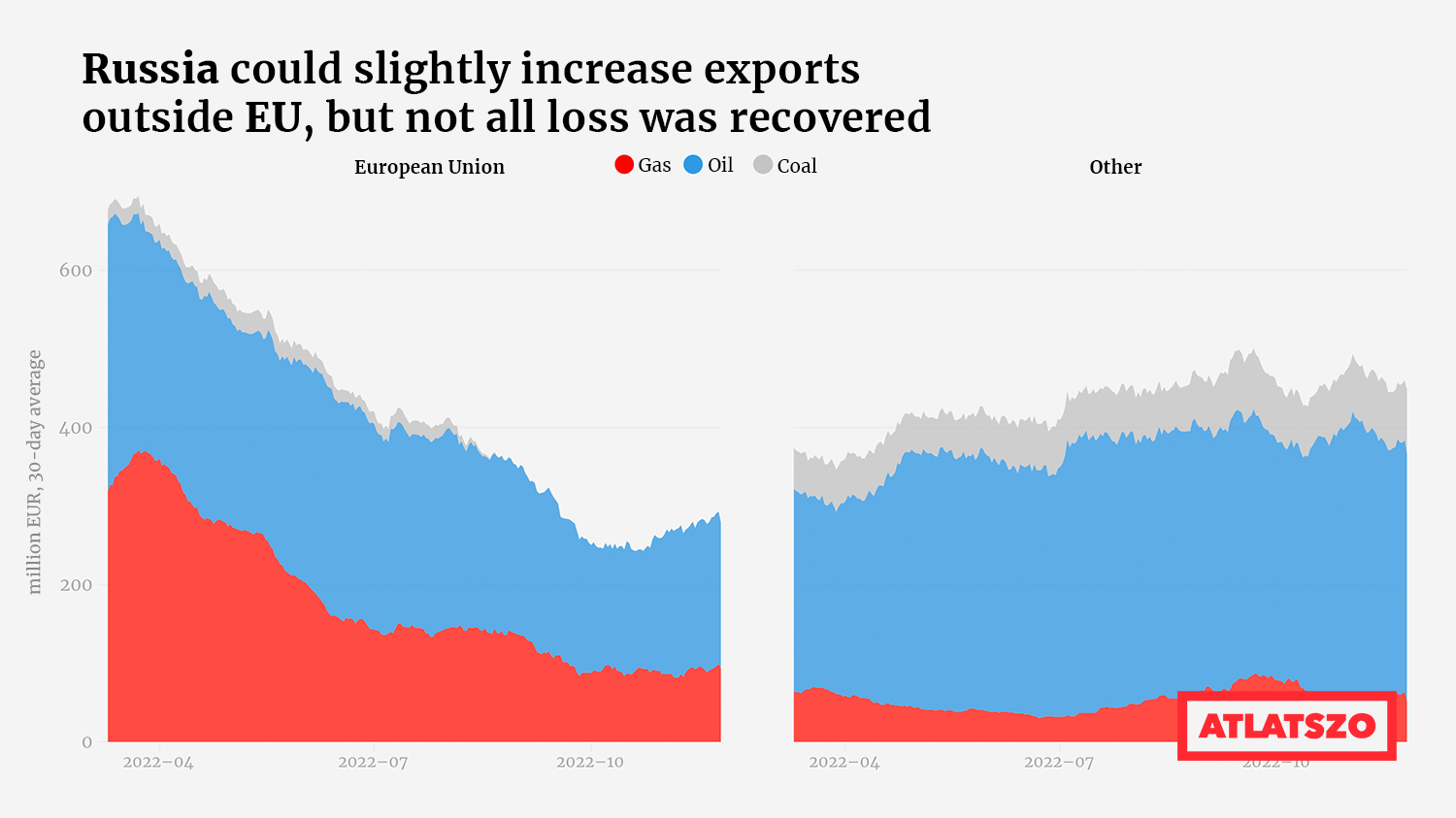

How has the embargo affected Russian oil imports? The Russia Fossil Tracker, created by the Centre for Research on Energy and Clean Air (CREA), has been collecting data on Russia’s exports of oil, gas and coal to countries since the start of the Russia-Ukraine war. Prior to the oil embargo, Germany was the biggest importer of Russian oil in November, buying one and a half billion euros worth of Russian oil in a month.

By imposing the sanctions, the EU has cut itself off from significant sources of oil. Russia supplied 29 percent of the EU’s oil needs in 2020, 42 percent of the country’s annual production. The EU could offset the Russian shortfall by increasing imports from other sources, but the US and Kazakhstan could also help make up for the 1.1 million barrels a day that no longer comes from Russia because of sanctions.

2. Gas supplies

The second question is about another major Russian energy source: Russian gas. Although the energy crisis that started at the end of 2021 pushed up the price of natural gas to unprecedented levels, Russian gas has been flowing almost uninterrupted to the continent.

As in the case of oil, Hungary would also oppose possible gas sanctions.

While 44 percent of the country’s 87 percent of imported oil needs came from Russia in 2020, Russia alone serves the country’s 67 percent dependence on gas imports.

The EU’s objective this year was not to sanction Russian gas, but to fill storage as soon as possible in preparation for the winter heating season.

In Hungary, gas consumption in October was 41% lower than in 2021, partly due to mild weather and partly due to higher utility costs. The market price of gas has fallen back to its end-2021 level following the refilling of storage, so if gas from Russia continues to arrive during the winter, this heating season will be manageable – at least in Hungary. And if the Russian gas supply were to stop, the gas stored in Hungary would still be able to meet national needs for this season.

It is expected that next year the European Council will add the sanctioning of gas imports to its list, so the EU’s goal for next year will be to secure other sources of gas besides refilling storage.

3. Solid fuels

The third question is about the ban on coal and other solid fossil fuels, which came into force on 10 August, as agreed in the fifth package of sanctions. In 2020, the EU produced 12 percent of its electricity needs from coal-fired power plants, with slightly more than half of the coal imported by the continent, including 55.6 percent from Russia.

As with oil, Hungary imports coal from several sources. Most of the 96.7 percent dependence is served by the United States (49.6 percent), with Russia in second place (21.7 percent).

The coal embargo, was considerably easier to implement than the oil or gas embargo. According to Bruegel’s analysis, coal can be easily substituted by other countries: in 2020, 17.7 percent of coal entering the EU came from the US, 13.7 percent from Australia and 8.2 percent from Colombia. But sourcing from alternative sources will not be cheap. The Rotterdam coal price, like other energy sources, went through a significant price rise at the end of last year, and at the start of the war the price skyrocketed and remained so for most of the summer.

In addition, the sanctioned country has also adapted particularly well to the new trade division, with Russia successfully expanding its markets in Turkey, China and India.

4. Nuclear fuel elements

According to the fourth question, the European Parliament also wants to sanction nuclear fuel, which would limit the fuel needs of some of Europe’s nuclear power plants, “jeopardising stable electricity supplies and raising prices.” Imports of nuclear fuel have so far not been included in any of the sanctions packages, nor is a future embargo planned.

There are 106 operating nuclear reactors in the EU, in 13 of the 27 Member States, most of them in France, with 56 (52%). Nuclear power plants supplied a quarter of the EU’s annual electricity demand in 2020. In Hungary, the Paks NPP has four operating reactors, which accounts for one third of the 2021 demand.

What supply alternatives could the EU have if Russia were to stop supplying nuclear fuel or equipment, or if sanctions were imposed on this type of energy? In 2021, Russia was only the third largest supplier to the continent, with Niger and Kazakhstan providing a larger share of fuel to the EU in recent years. So, in addition to increasing imports from countries that now account for a larger share than Russia, a revival of Australian imports, which have been stagnant and declining since 2012, could also meet demand for many of the continent’s reactors.

5. Russian investments

The fifth question also targets nuclear energy production, but from the investment side: „Many want to extend nuclear sanctions to the expansion of the Paks nuclear power plant. The European Parliament and some opposition parties also say that development cooperation with Russian companies should be halted.”

The government has made it clear that Hungary won’t support sanctions on the Russian nuclear industry. However, the the HUF 3,700 billion investment, which is classified for 30 years, is not the only newly strengthened tie between Russia and Hungary. In September last year, we signed a fifteen-year gas purchase contract with Gazprom, covering the purchase of 4.5 billion cubic metres of gas per year, which was extended on 31 August this year to include the purchase of a further 700 million cubic metres of gas. The government is keeping the content of the contracts and the exact terms secret.

6. Tourism

As part of the second package of sanctions (25 February), the Council voted to suspend visa facilitation rules for diplomats, other officials and business people. This was extended to all Russian citizens on 9 September. In the third package (28 February and 2 March), a ban on flights by Russian airlines and private aircraft was also imposed.

The sixth question is focusing on the loss of Russian tourists due to the sanctions and the negative impact on Hungarian tourism, which has not been able to return to pre-COVID-19 levels. In the year of the pandemic, tourism in Hungary dropped significantly due to the restrictions.

Data of the Hungarian Central Statistical Office (KSH) show that while the number of Russian travellers choosing Hungary increased slightly before the pandemic, it has been a fraction of the total in the last 13 years accounting for only 0.3 percent of all travellers from Russia in 2021. The absence of 200-300 thousand Russians who had previously visited did not break tourism.

7. Food supply, migration

The seventh and last question deals with the impact of sanctions on food supply and its possible migration consequences. As a consequence of food shortages and price increases due to war, it assumes that this will have a negative impact on developing countries, increasing the risk of famine and thus „leading to even greater migration flows than before and increasing pressure on Europe’s borders”. This revisits the previous narrative of the migration crisis, which the Fidesz government has often used since 2015.

The European Council’s website specifically points out that the sanctions do not affect exports of food, agricultural products or fertilisers, which are explicitly excluded from the scope of the sanctions. However, the price increase was significant for fertiliser prices, as well as for wheat, maize and soybeans (exceeding 2008 prices), but not only due to supply problems around fertilisers. According to the European Council, „Russia alone is responsible for the global food crisis”.

David Beasley, chairman of the UN World Food Programme, said that prolonged supply shortages could trigger a new wave of African migration to Europe. At the moment, however, there is no sign of North Africa or the Middle East heading to Europe. According to UNHCR, there has been no significant increase in mass migration to Europe since the war.

Are the sanctions working?

The EU is on the road to independence from Russia. Whether the war ends next year or not, this trend will continue, probably by cutting off imports of other energy sources such as gas or nuclear fuel. In addition, significant resources will be devoted to building a new supply chain, increasing domestic extraction and processing of raw materials and reducing energy demand. If the EU can use the coming year to achieve these goals, a more serious economic crisis than the one we are currently facing could be avoided on the continent.

So the question remains: are the sanctions working? Some of the data suggest that Russia has been weakened, but not yet completely broken by the EU’s sanctions policy, and has already established alternative markets in some of the sanctioned areas. But if the EU persists with restrictions, Russia will feel the impact of sanctions. This year, the country is already expected to receive $70 billion less per year than before the war, and the shortfall could be even higher in the future.

Translated by Zita Szopkó. The original, more detailed Hungarian versions of this story was written by Krisztián Szabó and are available here and here.

Share:

Your support matters. Your donation helps us to uncover the truth.

- PayPal

- Bank transfer

- Patreon

- Benevity

Support our work with a PayPal donation to the Átlátszónet Foundation! Thank you.

Support our work by bank transfer to the account of the Átlátszónet Foundation. Please add in the comments: “Donation”

Beneficiary: Átlátszónet Alapítvány, bank name and address: Raiffeisen Bank, H-1054 Budapest, Akadémia utca 6.

EUR: IBAN HU36 1201 1265 0142 5189 0040 0002

USD: IBAN HU36 1201 1265 0142 5189 0050 0009

HUF: IBAN HU78 1201 1265 0142 5189 0030 0005

SWIFT: UBRTHUHB

Be a follower on Patreon

Support us on Benevity!